DISP App 4 Annex 1 Assumptions for calculation of redress

1This Annex belongs to DISP App 4.4.

1 |

Assumption updates |

||||

1.1 |

R |

(1) |

A firm must use the following assumptions which are updated quarterly: |

||

(a) |

the RPI inflation rate; |

||||

(b) |

the CPI inflation rate; |

||||

(c) |

the post-retirement discount rate; and |

||||

(d) |

the pre-retirement discount rate. |

||||

(2) |

Redress calculations must be based on the new assumptions available on the first day of each new quarter, using publicly available data from the final business day of the quarter immediately before. |

||||

(3) |

Firms must use the updated mortality assumptions in DISP App 4 Annex 1 at 10.1G from 1 April each year. |

||||

2 |

Alternative assumptions |

||||

2.1 |

R |

A firm must not use assumptions that are less conservative than those specified in DISP App 4 Annex 1 . Where this appendix does not address the particular and individual circumstances of a consumer’s complaint, a firm should address those circumstances in accordance with the guidance at DISP App 4.2.5G. |

|||

2.2 |

G |

Where a consumer is likely to be disadvantaged by applying a pre-retirement discount rate calculated in accordance with DISP App 4 Annex 1 8.1G, firms should apply an appropriate alternative discount rate which reasonably reflects the expected rate of return from the consumer’s DC pension arrangement investments to avoid that disadvantage. |

|||

3 |

RPI inflation |

||||

3.1 |

G |

(1) |

A firm should use the RPI inflation rate which is based on the ‘UK instantaneous implied inflation forward curve (gilts)’ published by the Bank of England by taking: |

||

(a) |

the spot rate for the number of integer years to retirement, for a pre-retirement RPI inflation rate; or |

||||

(b) |

a derived forward rate commencing from the date of retirement for the number of integer years indicated by the discounted mean term, for a post-retirement RPI inflation rate, using the approach set out in DISP App 4 Annex 1 7.1G. |

||||

(2) |

A firm should use the 40-year rate where the number of integer years exceeds 40. |

||||

(3) |

A firm should use the rate for the shortest term available on the curve (including half-years) where the number of integer years required is fewer than shown in the curve. |

||||

(4) |

A firm should deduct an inflation risk premium of 0.2% from the pre-retirement RPI when deriving a RPI inflation rate for pre-retirement revaluation increases and the pre-retirement discount rate (but not for post-retirement increases). |

||||

(5) |

A firm should round the RPI inflation rate to the nearest 0.05% unless it is being used to derive another assumption. |

||||

4 |

Consumer Price Index (CPI) inflation |

||||

4.1 |

G |

(1) |

A firm should deduct an unrounded CPI adjustment factor from the unrounded RPI inflation rate, then round the resulting CPI inflation to the nearest 0.05%. |

||

(2) |

A firm should derive the pre-retirement CPI adjustment (to apply to the pre-retirement RPI rate) as follows: |

||||

(a) |

if 20YY + a ≤ 2030, an adjustment of 1.0%; or |

||||

(b) |

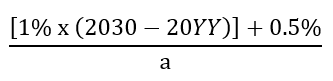

if 20YY + a > 2030, an adjustment determined by the result of the formula:

where: |

||||

(i) |

the calculation has a valuation date in year 20YY; |

||||

(ii) |

the consumer has a term to retirement of x years where: a ≤ x < b (and a and b are the integer values either side of x); and |

||||

(iii) |

a > 0 (as the pre-retirement inflation assumptions are not required when a=0). |

||||

(3) |

A firm should derive the post-retirement CPI adjustment (to apply to the post-retirement RPI rate) as follows: |

||||

(a) |

if 20YY + a > 2030, a rate of 0%; or |

||||

(b) |

if 20YY + a ≤ 2030, a rate determined by the result of the formula: where: |

||||

(i) |

the calculation has a valuation date in year 20YY; |

||||

(ii) |

the consumer has a term to retirement of x years where: a ≤ x < b (and a and b are the integer values either side of x); and |

||||

(iii) |

the consumer retires at an age with associated discounted mean term of d. |

||||

5 |

Earnings inflation |

||||

5.1 |

G |

A firm should use earnings inflation of CPI + 1% whenever they need to project benefits which are earnings related, such as those which increase in line with an order made under section 148 of the Social Security Administration Act 1992, by: |

|||

(1) |

taking the relevant CPI spot inflation rate, derived in line with the (unrounded) approach for setting the CPI assumption; and |

||||

(2) |

rounding the resulting earnings inflation rate to the nearest 0.05%. |

||||

6 |

Pension increases in payment |

||||

6.1 |

G |

(1) |

Where a pension tranche increases in payment with either RPI or CPI and the scheme rules impose a cap and/or a floor, the pension increase assumption should be derived using a standard Black Scholes model with an inflation volatility of 1.0%. |

||

(2) |

The final assumption in (5.1G(1)) should be rounded to the nearest 0.05%. |

||||

7 |

Post retirement discount rate |

||||

7.1 |

G |

To calculate the initial post-retirement discount rate, firms should: |

|||

(1) |

determine the relevant rate on the Bank of England nominal government bond (gilt) yield curve, using the following formula:

where: |

||||

(a) |

r is the spot rate for a term equal to the sum of the integer period to retirement and the relevant discounted mean term; |

||||

(b) |

rs is the spot rate for the integer period to retirement; |

||||

(c) |

n is the integer number of years to retirement; and |

||||

(d) |

d is the discounted mean term; |

||||

(2) |

derive an ‘initial rate’ by deducting 0.6% from the rate in (1) above, as an allowance for annuity pricing margins. |

||||

7.2 |

G |

(1) |

Where the consumer’s presumed date of retirement is after the valuation date, firms should use the discounted mean term in the table below based on the consumer’s age at the presumed date of retirement; otherwise, they should use the discounted mean term based on the consumer’s age at the valuation date: |

||

Age |

Discounted mean term |

55 |

23 |

60 |

20 |

65 |

16 |

70 |

13 |

75 |

11 |

(2) |

Where the consumer’s age is in between the ages shown in the tables, firms should use linear interpolation to derive the discounted mean term, and round the resulting figure to the nearest integer. |

||||

(3) |

Where the consumer’s age is higher than the ages shown in the tables, firms should derive the discounted mean term by extrapolation, and round the resulting figure to the nearest integer. |

||||

7.3 |

G |

Where the consumer’s date of retirement is after the valuation date, firms should derive a final post-retirement rate, as follows: |

|||

(1) |

(a) |

75% of the initial rate, plus; |

|||

(b) |

25% of the initial rate plus 1.6%; or |

||||

(2) |

by modifying the approach in DISP App 4 Annex 1 7.3G(1) to reflect where a pension commencement lump sum was payable in addition to the pension income in the defined benefit occupational pension scheme. |

||||

7.4 |

G |

Firms should round the final post-retirement rate to the nearest 0.05%. |

|||

8 |

Pre-retirement discount rate |

||||

8.1 |

G |

(1) |

Where the retirement date is after the valuation date, the pre-retirement discount rate represents the assumed rate of return for the period from the valuation date to the consumer’s retirement date and targets a rate of return of one-half of the return on equities. |

||

(2) |

A firm should round down the period of retirement to the number of integer years remaining to the retirement date. |

||||

(3) |

A firm should derive the pre-retirement discount rate as follows: 0.5 x [(1 + CPI spot inflation rate) x (1+ average dividend yield) x (1 + growth in dividends) - 1] where: |

||||

(a) |

the CPI spot inflation rate is derived in line with the (unrounded) approach for setting the CPI assumption; |

||||

(b) |

the average dividend yield is taken as the arithmetic average of the dividend yield on the FTSE All Share Index of the last business day over the last 4 quarter ends; and |

||||

(c) |

the growth in dividends is assumed to be 1.0 % each year. |

||||

(4) |

Firms should round the final assumption to the nearest 0.05% per annum. |

||||

9 |

Charges |

||||

9.1 |

G |

(1) |

Default product charges: 0.75% each year. |

||

(2) |

Default ongoing adviser charges: 0.5% each year. |

||||

(3) |

Default initial adviser charges: 2.4% of investment value. |

||||

(4) |

Minimum initial advice amount: £1,000. |

||||

(5) |

Maximum initial advice amount: £3,000. |

||||

10 |

Demographic assumptions |

||||

10.1 |

G |

A firm should use pre and post-retirement mortality assumptions based on: |

|||

(1) |

the year of birth mortality rate derived from each of the Institute and Faculty of Actuaries’ Continuous Mortality Investigation tables PMA16 and PFA16 and including mortality improvements derived from each of the male and female annual mortality projection models, in equal parts; and |

||||

(2) |

mortality improvements derived from the male and female annual CMI Mortality Projections Models in the series CMI (20YY-2) M_[1.25%] and CMI (20YY-2_F)_[1.25%] in equal parts for the year commencing 1 April 20YY. |

||||

10.2 |

G |

A firm should use the actual age of a spouse or civil partner who is eligible for benefits on the consumer’s death unless their age is unknown, in which case the firm should assume they are the same age as the consumer. |

|||

10.3 |

G |

(1) |

Where the presumed date of retirement is after the valuation date, firms should use the consumer’s current marital/civil partner status to determine which status to use at the presumed date of retirement, using the table below: |

||

Term to retirement (in years) |

Married/Civil partner |

Not married/No civil partner |

0 |

100% |

0% |

5 |

95% |

10% |

10 |

90% |

20% |

15 |

85% |

30% |

20 |

80% |

40% |

25 |

75% |

45% |

30 |

70% |

50% |

35 |

70% |

55% |

40 |

70% |

55% |

(2) |

When deriving status rates from the table in (1), firms should: |

||||

(a) |

interpolate for terms that are not shown and round to the nearest 1%; and |

||||

(b) |

not apply any adjustments for mortality of the spouse/civil partner before the retirement date. |

||||

(3) |

Where the retirement date is prior to the valuation date, a firm should use the consumer’s actual marital/civil partner status, at the valuation date, where known. |

||||

(4) |

Where the actual marital/civil partnership status is not known, a firm should use the assumption that the consumer is not married or in a civil partnership. |

||||

11 |

Default factors for early retirement, late retirement and lump sum commutation |

||||

11.1 |

G |

Where the date of retirement is at or prior to the valuation date and the actual early retirement factors are unknown, firms should use a default early retirement factor of 4.0% per annum compound, applied after the pension has been revalued to the assumed date of retirement, and assuming the factor is compounded for the number of years, n, to retirement as follows: (1 – 0.04)n. |

|||

11.2 |

G |

Where the consumer has already passed their normal retirement age and the actual late retirement factors are unknown, firms should use a default late retirement factor of 5.0% per annum compound, applied after the pension has been revalued to the late date of retirement. |

|||

11.3 |

G |

Where the date of retirement is prior to the valuation date and the actual lump sum commutation factor is unknown and cannot be reasonably determined from other available information, firms should use a default lump sum commutation factor of 20. |

|||

12 |

Accumulation rate for rolling up past payments to the valuation date |

||||

12.1 |

G |

To calculate the accumulated value of past payments at the valuation date, a firm should ensure the accumulation rate from the date of payment to the valuation date reflects the cumulative return, as if each payment had been invested in line with the Bank of England Base Rate over the period. |

|||

12.2 |

G |

The cumulative return for each past payment should reflect changes in the Bank of England Base Rate over the period by compounding the relevant rates over the period, using the following approach: where: t is the number of different Bank of England Base Rates that applied over the period from the date of payment of a past payment to the valuation date; it is the Bank of England Base Rate, for each t; and nt is the number of days that each Bank of England Base Rate applies in the period. |

|||

13 |

Cash enhancement rate of return |

||||

13.1 |

G |

The cash enhancement rate of return is: 50% of the return on the FTSE 100 Total Return Index. |

|||

14 |

Additional compensation sum |

||||

14.1 |

G |

Where the date of retirement is after the valuation date, firms should increase the redress amount using a rate equal to the pre-retirement discount rate (with an adjustment for charges) between the valuation date and the payment date. |

|||

14.2 |

G |

Where the date of retirement is at or prior to the valuation date, firms should increase the redress amount using a rate equal to the post retirement discount rate (with no adjustment for annuity pricing or pension commencement lump sums) between the valuation date and the payment date. |

|||

14.3 |

G |

To calculate the additional compensation sum, firms should derive a factor as follows: (1 + r)t/365 Where: r is the rate in DISP App 4 Annex 1 14.1G or 14.2G, as appropriate; and t is the number of days from the valuation date to the payment date, not counting the payment date itself, and where the valuation date is Day 1. |

|||

15 |

Free standing additional voluntary contributions comparator returns |

||||

15.1 |

G |

The benchmark index for the rate of return within an in-house additional voluntary contribution arrangement is: |

|||

(1) |

the CAPS ‘mixed with property’ fund, for returns prior to 1 January 2005; and |

||||

(2) |

the FTSE UK Private Investor Growth Total Return Index for returns from 1 January 2005. |

||||

16 |

Correct comparator scheme |

||||

16.1 |

G |

(1) |

For the purpose of this appendix, the firm must treat a consumer as having a defined benefit occupational pension scheme if immediately before the pension transfer or pension conversion the consumer had rights in a defined benefit occupational scheme but would now be entitled to rights or benefits from any of the following if they had not been transferred or converted: |

||

(a) |

the Pension Protection Fund, whether during an assessment period or after the entry of the ceding defined benefit occupational pension scheme; or |

||||

(b) |

any registered pension scheme offering safeguarded benefits. |

||||

16.2 |

G |

(2) |

If there is more than one defined benefit occupational pension scheme that the consumer could have had rights in if they had not transferred to the DC pension arrangement, the firm should calculate the primary compensation sum using the defined benefit occupational pension scheme that the consumer would most likely have had rights in if the firm had provided compliant pension transfer advice. |

||

(3) |

When determining which defined benefit occupational pension scheme the consumer would have had rights in, the firm should consider all of the evidence available to it and which it could reasonably obtain. |

||||

(4) |

If the defined benefit occupational pension scheme used by the firm when calculating redress is likely to produce a primary compensation sum that is lower than would be the case if another defined benefit occupational pension scheme had been used, the firm should explain: |

||||

(a) |

why the firm considers the redress offer would be higher if another defined benefit occupational pension scheme had been used as the comparator; |

||||

(b) |

why it considers the consumer would most likely have had rights in the defined benefit occupational pension scheme used over other options; |

||||

(c) |

the evidence and information considered by the firm when determining which defined benefit occupational pension scheme to use when calculating the primary compensation sum; and |

||||

(d) |

how the consumer can challenge the defined benefit occupational pension scheme used by the firm if they disagree with the firm’s decision. |

||||

(5) |

For consumers who were members of the British Steel Pension Scheme, firms should determine the correct comparator scheme to use in accordance with CONRED 4 Annex 21 13.21R to 13.26R. |

||||